|

The capital budget includes major infrastructure projects such as roads, vehicles/equipment, parks, sidewalks, trails, streetlights, playgrounds and buildings. It includes both the development of new, and the maintenance/rehabilitation of existing infrastructure.

Examples of Capital Expenses

- Roads

- Buildings

- Fleet

- Equipment & Furnishings

- Computer hardware and software

- Studies

|

| What is a budget? |

|

Merriam-Webster Dictionary: “A statement of the financial position of an administration for a definite period of time based on estimates of expenditures during the period and proposals for financing them.”

A Capital Budget and Forecast is where the Township plans for upcoming years and identifies how to pay for Township infrastructure projects, such as road reconstruction, park improvements and public buildings.

The Operating Budget encapsulates the Township's plans for day-to-day operations, including salaries, utilities and supplies to deliver Municipal services.

|

| How is the budget prepared? |

|

The Annual Budget is a continuous, integrative process that takes several months to complete. The budget draws information from a wide range of sources and is an integrated process that encapsulates the Township's services, service levels, policies, public input and plans into a consolidated financial road map.

There are many factors that inform the budget process annually, including:

- Economic Indicators

- Public Requests

- Council Requests

- Policies

- Risk Mitigation

- Staff Input

- Masterplans/Strategies

- Inflation

- Legislation

- Development Activities

The Township uses a combination of both Traditional and Zero-based Budgeting when preparing the annual budget.

Traditional Budgeting - a technique in which all expenses are based on the previous year’s budget and are reviewed/adjusted annual based on inflationary impacts, new expenditures/revenue.

Zero-based budgeting – a technique in which all expenses must be justified for a new period or year starting from zero versus starting with the previous budget and adjusting it as needed

While preparing the 2025 budget, a combination of traditional and zero-based budgeting is utilized. Traditional budgeting is used for items such as materials and supplies, user-fee revenues as without historical trends the amounts are indeterminable. Zero-based budgeting is utilized for expenditures such as salaries and benefits, insurance and grant revenue as the amounts are independent from previous years.

|

| What makes up a budget? |

|

The Operating Budget includes all of the expenditures (e.g., wages/benefits, supplies, contracted services, utilities, etc.) required to deliver day to day Township services. It also includes the non-tax revenues that we receive (e.g., ice rentals, interest income, planning and development fees, etc.).

The Operating Budget for the Town consists of 6 main departments with numerous functional activities in each. The operating budget is prepared based on existing service levels which are then adjusted for the cost of supporting new growth in the Township (i.e., providing services to the new homes and businesses) and legislative requirements. Its also includes a general levy funded contribution to Reserve/Reserve Fund Allocations to support future capital expenses.

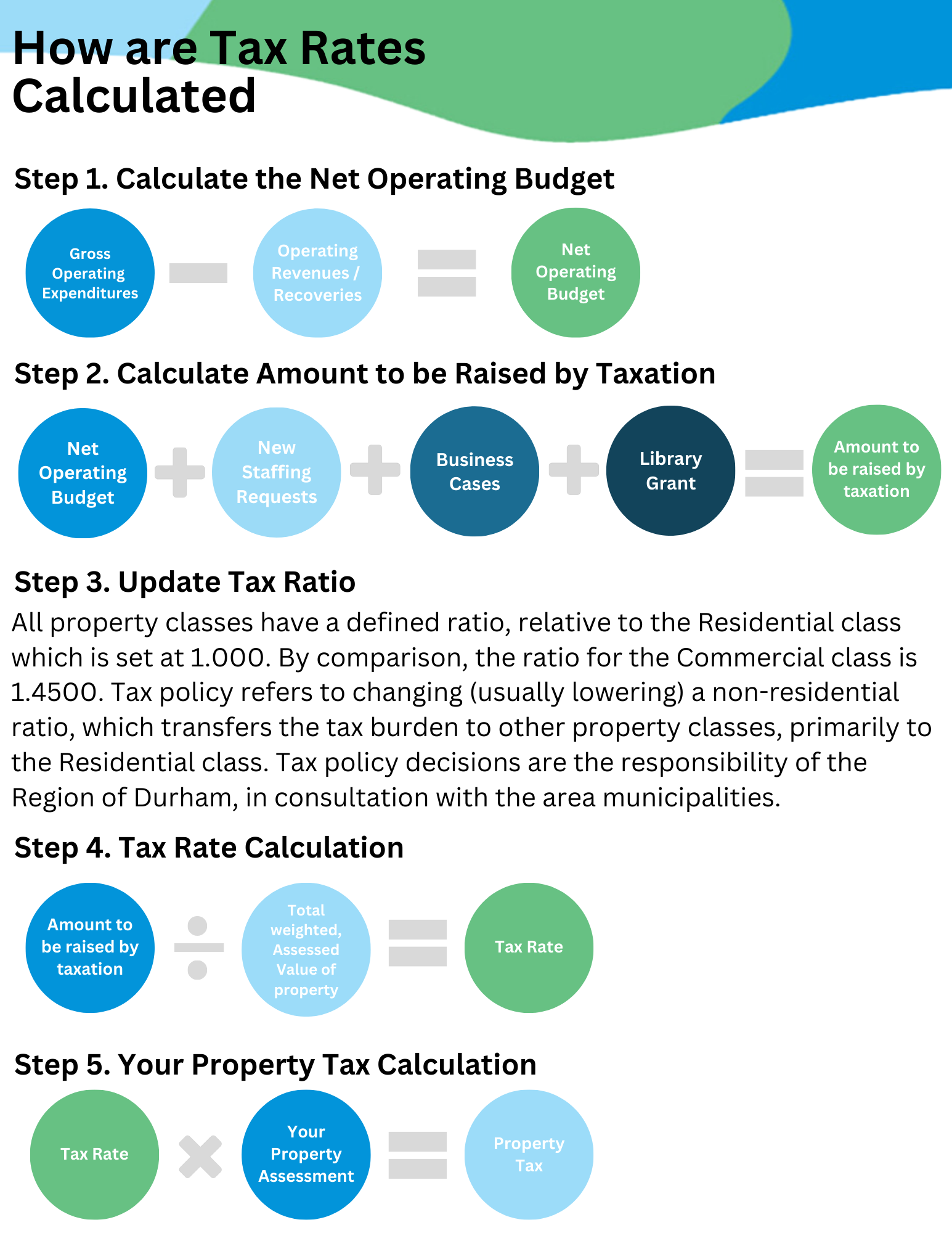

The amount to be raised from taxation is based on the approved Net Operating Budget, which is calculated as the Gross Operating Expenditures less Operating Revenues/Recoveries received from non-tax sources (such as user fees, fines, interest income, Ontario Municipal Partnership Funds and other grants, etc.)

The Capital Budget includes one-time expenditures for major projects (often referred to as “infrastructure”) such as roads, vehicles/equipment, parks, trails, playgrounds and buildings; as well as studies and information technology. It includes both the development of new and the maintenance/rehabilitation of existing infrastructure. The capital budget covers a one-year period (the upcoming budget year)

The funding for capital projects comes from a wide range of different sources, with the most common ones listed below:

- Development Charges

- Reserves and Reserve Funds

- Canada Community-Building Fund

- Ontario Community Infrastructure Fund

- Other grants, donations and external funding sources

|

| How is the Library funded? |

| The Beaverton, Cannington and Sunderland libraries operates independently from the Township of Brock (under one Library CAO), however the grant provided by the Township to the Libraries accounts for approximately 90% of the Library’s annual operating budget. One member of Council sits on the Library Board and participates in the Board’s decision making processes. The Board provides reports to Township Council as required throughout the year and provides their annual grant request as part of the Township’s budget process. |

| What is a reserve? |

|

Financial reserves are an effective tool to support municipal asset management planning, as they allow for funds to be set aside to manage assets throughout their lifecycle.

Municipal reserves are not a measure of wealth, but rather are a planning tool.

Municipalities are not permitted to run deficits, therefore, reserves allow municipalities to save money for major infrastructure projects.

Municipalities are permitted to finance capital projects with debt, however, the amount of debt municipalities may incur is limited and the high cost of debt maintenance may not be attractive in certain circumstances.

There are different type of reserves held by municipalities and each are for different purposes. These include:

Discretionary Reserve Fund: A reserve fund created at the discretion of Council whenever revenues are earmarked to finance future expenditures

Obligatory Reserve Fund: A reserve fund that is required by legislation or agreement for a special purpose

|

| How are house values assessed? |

If you have questions about your assessment, call MPAC at 1-866-296-6722 or visit the MPAC website(External link)(External link). For property-specific inquiries, visit the About My Property(External link)(External link) section to view information on your property, access your property assessment notice, and compare your property to others. If you disagree with your assessment, you can file a Request for Reconsideration (deadlines applicable). |

|

Why are municipal tax rate increases often higher than the rate of inflation?

|

|

When people talk about inflation, they are usually referring to Statistics Canada’s Consumer Price Index (CPI), a theoretical “shopping basket” of consumer goods. Unfortunately, CPI does not reflect the cost increases that all municipalities face for expenditures such as contracted goods/services, utility costs for streetlights and large facilities, insurance, building materials, asphalt, concrete, etc. Increases for these types of items are typically much greater than standard CPI increases and these are the goods that municipalities are required to purchase.

|

| What are User Fees? |

|

Many services offered to residents are available equally to all and these would be included as part of your property taxes. Examples include Fire protection, snow plowing of roads, grass cutting in parks etc. User fees are the rates charged for the delivery of products or services to residents that are optional and offered on a fee for service basis. Examples include rental of meeting rooms, purchase of a permit, enrollment in a day camp program etc.

|

| Do user fees cover the cost of the service? |

|

No this is not always possible. Although these fees are reviewed annually and compared against other areas and similar municipalities, staff balance the recovering of charges and ensuring that programs and services are offered to the public in an affordable and responsible manner.

|

| Do Development Chargers cover the entire cost of the capital project required for new development? |

|

No. But we are getting closer. Provincial legislation, specifically the Development Charges Act, requires municipalities to contribute to certain development projects. Other legislative requirements can further increase the amount a municipality must contribute. While recent legislative changes have broadened the scope of project costs that can be recovered through Development Charges, certain capital items such as administration buildings and the acquisition of parkland, are exempt and must be 100% paid for by taxpayers.

|

Why do my total taxes sometimes increase more than the Township's Tax Rate increase?

|

The Township only controls 38% of the total tax bill, with the Region responsible for 50% and the final 12% controlled by the Province for education. If the Region and/or Provincial increases are higher than the Township’s, then your total increase will be higher than the Township’s increase.

Also, a reassessment related increase (where the value of your property is increasing at a faster rate than the average for the whole municipality) may cause your total tax increase to be higher.

|

How is the Township using the Canada Community Building (previously Federal Gas tax) Funding they get from the Federal Government

|

|

In 2005, all municipalities signed an agreement in order to receive the Federal Gas Tax fund which was updated in April 2014 and is in place until 2023. The government recently changed the name of this grant to the Canada Community Building Fund.

In 2023, the Township budgeted to receive $466,200 from the Canada Community Building Fund to be used to assist with the following projects:

- Energy Conservation Demand Management Plan

- Asset Management Plan Strategy & Update

- Facility improvements to the Sunderland, Cannington and Beaverton Fire Stations

- Playground Equipment

- Facility improvements to the Foster Hewitt Memorial Community Centre

- Facility Improvements to the Rick MacLeish Memorial Community Centre

- Facility improvements to the Sunderland Memorial Arena

- Facility improvements to the Sunderland Historical Society Building

- Building Assessments and Cost Studies (various locations throughout the Township)

- Road Needs Assessment

- Bridges and Culverts Needs Assessment

|

|